USD-INR JUN

INR has traded with a weakening bias as less dovish market

expectations for Fed policy has boosted the USD and US

rates, pressuring India's ability to fund its current account

deficit. Though oil and gold prices have eased, the external

deficit is unlikely to fall enough to nullify external funding

risk for the rupee, particularly if the market's bias for pricing

in a less dovish Fed to the USD continues. Capital account

inflows following policy rate cuts have thus far failed to

support the INR on a sustained basis.

EUR-INR JUN

Stronger dollar, an ECB interest rate cut, a building

discussion on the potential of negative interest rates and a

large EUR short position (reported by the CFTC).

JPY-INR JUN

In May the yen reached a 4.5 year low having been

pressured by aggressive Bank of Japan policy juxtaposed

against rising expectations that the Fed would begin

stepping away from QE.

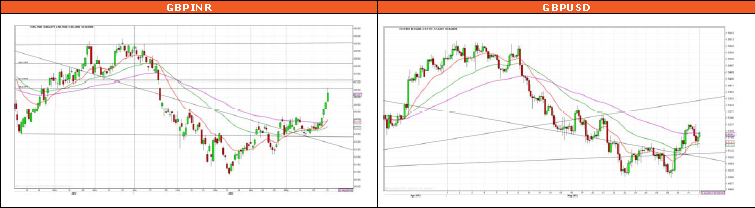

GBP-INR JUN

Bearish technicals and a broadly stronger USD all

contributed to GBP weakness in May. Outlook remain bearish

viewing the combination of low growth, elevated inflation, an

upcoming change in leadership at the BoE and negative

sentiment as GBP negatives.

Latest Update

The Reserve Bank of India continues to provide monetary stimulus, although at a cautious pace, in order to stimulate sluggish economic activity; on May 3rd,

monetary policymakers lowered the benchmark repo rate by 25 basis points (bps) to 7.25%, taking cumulative reductions to 75 bps since the beginning of the

easing cycle in January. The authorities identified two key factors behind the decision: a continuous and steep deceleration in economic growth, and an easing

in WPI inflation closer to the central bank’s tolerance threshold. While the policymakers pointed out that there is little space for further monetary easing,

market assess that the fact that wholesale price inflation weakened substantially to 4.9% y/y in April from 6.0% the month before will allow further modest

reductions in the benchmark interest rate. India’s economic performance remains subdued, challenged by a high cost of financing, constrained fiscal room and

subdued global demand conditions. A gradual improvement is in sight, however, supported by monetary easing and the government’s attempt to implement

modest economic reforms. Market is rumored with revised India’s real GDP growth forecasts downwards and now expect the economy to expand by 5½% in

2013, followed by a 6% gain in 2014. Shifts in investor sentiment will continue to be reflected in the value of the Indian rupee, as the country suffers from a

large current account deficit (equivalent to around 5% of GDP in 2013), a negative sovereign credit rating outlook (affirmed by Standard & Poor’s in May),

weak government finances, and political instability.

Market Roundup

Global markets turned jittery after Congressional testimony by Fed Chairman Ben Bernanke and minutes from the FOMC's latest policy meeting

seemed to send conflicting messages. The markets were a bit flummoxed as the Chairman predictably cited "premature tightening" as a risk to the

recovery before saying later that the Fed could begin to dial-down purchases at "one of the next few meetings." However, the Fed minutes released

same day showed "a number of participants" are prepared to slow QE as soon as June.

U.S. initial jobless claims fell to 340,000, a decrease of 23,000 from the previous week's revised figure of 363,000. Economists had expected jobless

claims to drop to about 345,000. US new home sales climbed 2.3% to a seasonally adjusted annual rate of 454,000 in April from the revised March

rate of 444,000. Economists had expected new home sales to increase by 1.9%.

Eurozone consumer confidence indicator came in at -21.9, up from April's score of -22.3. Economists were expecting a reading of -21.8 for May. The

latest reading is the highest since July 2012. Eurozone composite output index, that measures performance of the both manufacturing and service

sectors, rose to 47.7 in May from 46.9 in April. Economists expected the reading to rise to 47.2. German composite output index rose to 49.9 in May

from a five-month low of 49.2 in April.

French Purchasing Managers' Index for the service sector held steady at 44.3, the manufacturing PMI rose to 45.5 from 44.4 in April. Economists had

forecast the services index to rise to 44.5 and manufacturing index to reach 44.7. The Economic and Monetary Union (EMU) is a more stable union

today than it was a year ago, European Central Bank President Mario Draghi said. Also "markets are fully confident that the euro is a strong and stable

currency," he said in a speech in London.

German Ifo index of business confidence rose to 105.7 in May from 104.4 in April and beat estimates of 104.5 reading.

China's HSBC flash PMI fell into contraction territory for the first time in seven months in May, dropping to 49.6 from 50.4 in April, missing

expectations. “The cooling manufacturing activities in May reflected slower domestic demand and ongoing external headwinds. A sequential slowdown

is likely in the middle of Q2, casting downside risk to China's fragile growth recovery. Moreover, the further signs of labor market slackness call for

more policy support. Beijing still has fiscal ammunition to do so." HSBC Markit said.

The Bank of Japan decided to keep its monetary easing program unchanged from that announced in April and said the economy has started to pick up.

EURO ZONE - First-quarter GDP figures released this month for the euro area highlighted the enduring economic weakness in the region. The

results fell short of market expectations, particularly in the case of Germany, where both investment and exports declined sharply during

January-March (just offset by an expansion in household spending and larger drop in imports). The ECB’s expected 2013 H2 recovery still

appears far off, and recessionary conditions could well persist into the second quarter. The fact that several key developed and emerging

markets also appear sluggish – prompting a new wave of monetary policy stimulus – suggests that global growth momentum is gathering

speed more slowly than earlier anticipated. Recent weeks have seen increasing acknowledgements by policymakers regarding the absence of

a forthcoming recovery and the inability of crisis-ridden states to return to growth amid severe fiscal austerity. Even the German Finance

Minister has called for urgent action on youth joblessness, championing proposals for bilateral aid agreements with Germany’s troubled euro

zone partners. A slight uptick in the PMIs in May was a welcome development, but may prove to be an aberration, in which case the ECB may

be compelled to implement another interest rate cut (following the quarter-point reduction to 0.50% in May). Inflation is expected to rebound

somewhat after a steep decline in April, though price pressures will remain subdued through 2014.

The pound showed renewed weakness in May, with losses amounting to roughly 3% versus the US dollar reflecting weak economic data and

the general bias toward USD strength over the month. Despite the rebound in output in the first quarter (the preliminary GDP estimate

confirmed growth of 0.3% q/q in January March, following the prior quarter’s 0.3% contraction), there are few indications that the economy is

entering a meaningful recovery. The gain was driven almost entirely by a large build-up in inventories, with a small addition from household

spending. Meanwhile, private investment and exports continued to detract from growth. Disappointing retail sales data for April suggest that

consumer spending is losing steam. The fact that the government’s promised ‘rebalancing’ toward investment and trade has yet to materialize

has prompted calls for a tempering of fiscal consolidation plans. According to the IMF’s latest Article IV Consultation report on the UK

(released May 22nd), of the GBP130 billion in deficit reduction measures slated for FY 2010/11 to FY 2015/16, more than half have already

been implemented. The report also supported an expansion of the Bank of England’s (BoE) asset purchase program and use of forward

guidance by the central bank, and stressed the return of the two state-intervened banks to private ownership in order to strengthen

confidence in the financial sector. Inflation dropped sharply in April, from 2.8% y/y to 2.4%. Much of the decline was due to temporary

factors, however, and is unlikely to cause any great shift in opinions at the BoE.

Market participants’ attention is centered on Japan’s economic performance in order to assess the effectiveness of the country’s recent

unprecedented monetary policy actions. Signs are emerging that policymakers’ revitalization efforts are starting to bear some fruit: earlier

improvements in confidence are translating into a pickup in household spending, while leading indicators point to increasing economic

momentum more broadly. In addition, the external sector should receive a boost from the recent substantial depreciation of the Japanese

yen. Nevertheless, an extended equity market correction could translate into deterioration in consumer and business confidence, potentially

erasing some of the recent improvements. The country’s real GDP increased by 0.9% q/q (non-annualized) in the first quarter of the year

following a 0.3% gain in the final three months of 2012. The growth was reasonably broadly-based with the exception of weak investment

activity. Market expect the economy to expand by 1.4% (1.0% previously), followed by a 1.5% gain in 2014. While the Japanese monetary

authorities seem determined to end deflation, inflation remains in negative territory for the time being (consumer prices declined by 0.9% y/y

in March). Market assess that the period of deflation will come to an end around mid-year, with inflation creeping gradually higher towards

1.2% y/y by the end of 2014. In light of the substantial monetary policy measures announced in April, market does not foresee any material

policy changes in the near term.

WHAT EVER YOU EARN FROM MY CALLS PLEASE GIVE 10% PROFIT'S FOOD TO COWS AND DOGS HELP THM GOD WILL HELP YOU-!!!